- Search Results

One of the things I am constantly looking for is how to improve the existing strategies if that is possible. I’m hoping other members will give their thoughts on how to create a strategy that improves your existing strategies. What tools do you use other than LI? Are you betting inflation will come in the future and want to create an inflation strategy? We are lucky that LI has done all the hard work and we don’t have to spend hours figuring out how to create new strategies. LI gives a 3 main categories of assets that are uncorrelated and a combined Hedge. There are other assets like tips and currency but the four main ones are below:

1. Equity

2. Bond

3. GLD

4. HedgeWhat if your crystal ball tells you that when inflation happens hard assets like commodities and precious metals will rise in price. You might want to create a Hedge strategy to lower volatility that uses precious metals or metals. Here is a process to create the strategy but I am sure there are better ways and lot’s of questions:

1. Select a precious metals ETF. I will start with PALL, GLD, SLV

a. A big question is will PALL rise when inflation hits? It is mostly used in gasoline catalytic converters. Therefore it might not.

b. Am I curve fitting by adding PALL since it has done so well over the last couple years?

c. Should you add more assets like URA?

d. How do you choose what assets are best for a strategy?

2. Look at the correlations between them and against Equities and Bonds using the following:

a. https://www.portfoliovisualizer.com/asset-correlations

3. The correlations only point you in the right direction. GLD, TLT are the most uncorrelated to SPY but PALL:SPY = 0.37 and SLV:SPY = 0.38.

4. Create the Strategy “Precious Metals” And optimize the parameters over 3 years.

a. Monthly Rebalance

b. 122 days lookback

c. Use top 2 ETF

d. Max allocation = 60%

e. Volatility Attenuator = 2.5

5. I choose these parameter settings based on the optimization giving stable returns across many lookback periods.

6. Add the strategy Precious Metals to the Strategy “0 LI Strategies of strategies”. This is done in the strategy manager.

a. Duplicate 0 LI Strategies of strategies

b. Rename the strategy “0 Test1” or anything you like.

c. Save it

d. Add Precious metals

7. Optimize 0 Test1 and choose parameters that have stability over a 3 year time period.

a. The optimization I only changed the lookback in the original strategy from 166 to 155 and Volatility Attenuator to 0.5.

8. Compare the results.

a. The New model 0Test1 has a better return but a slightly higher volatility.Questions and Next steps:

1. Did I curve fit by adding PALL? PALL has done very well over the last 3 years. If I added the uranium metal ETF URA it would not do as well. Selecting what ETF’s go in the strategy is critical. The objective of the strategy should drive this.

2. Does the increase in performance justify the increase in volatility?

3. Was 3 years a good time period to optimize across? Or should I use 5 or 10?

4. Let the model run OS for 3 years and then reevaluate it. This is the only way to really tell if the strategy works.

5. If there is no inflation it is possible that commodities and precious metals prices fall. I need to work on the crystal ball.In this process my goal was to lower volatility of an existing strategy, 0 LI Strategies of strategies. That goal was not achieved but it would be worth exploring other strategies that help reduce volatility in the future. If anyone would like to post their process for creating a strategy and how the assets are chosen please feel free to do so. LI seems to group similar assets into the strategy like US equity vs World Equity. Bond strategy vs Gold strategy. Then they combine them to optimize the KPI.

Cheers,

Mark V.Hi everyone

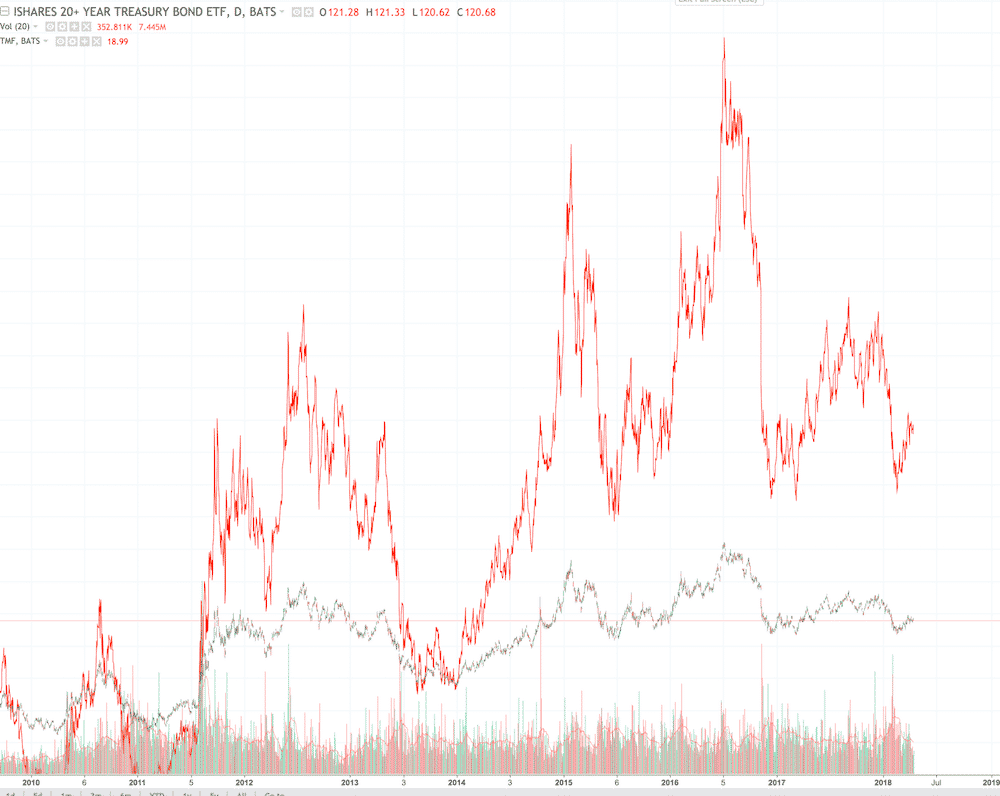

I’ve noticed that TMF has not been rising in response to falls in SPXL, or at least its response is muted. Additionally, it has had considerable downside recently.

In view of this, are there any other hedges we could be using?

Or perhaps moving out of leveraged products and into unleveraged SPY/TLT type trades (UIS)?

Have there been similar periods of hedges losing their inverse correlation to risk assets that we can draw some lessons from?

Thanks

I would like to discuss a strategy I have been working on and would welcome any feedback.

All my optimizations use a 5-year lookback period. I know there has been much discussion about this over the years and there does not appear to be firm consensus on the best period to use, however 5 years covers a good growth period and some good pullbacks in 2015, 2018 and 2020 so it feels to me to be a reasonable representative period.

Whenever I run the optimizer, I do not always use the red square. I try to find a good result square that also has good stable results for the 8 squares immediately around it.

I have not carried out any analysis using the volatility limit or the advanced QT settings.

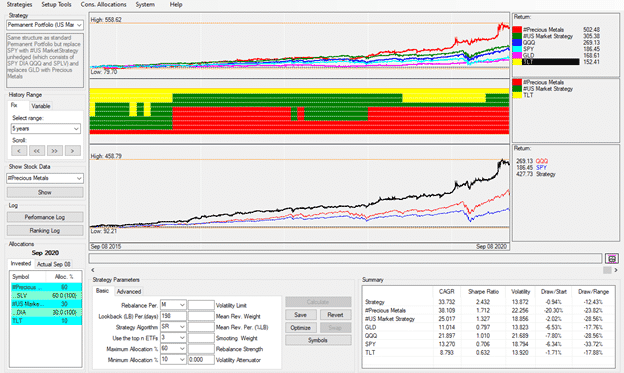

All the stats are based on data at the end of Sept 8th 2020.Starting Point Permanent Portfolio

My starting point was the Permanent Portfolio. I like that this is a very simple strategy that only uses three ETFs and is “self-hedging”. The 5-year results are CAGR = 11.192 with MaxDD = -17.38. My objective is to increase the CAGR to 20+ and reduce the MaxDD to better than -15.

I started off with finding a replacement for GLD and created a Precious Metals (PM) strategy that consisted of GLD, SLV, PALL, CPER, JJC and PPLT which gave much better results than GLD alone. On further analysis removing the worst performers (CPER, JJC and PPLT) gave much better results.

Incorporating my PM sub-strategy into the MPP with SPY and TLT also gave much better results so I knew I was heading in the right direction.

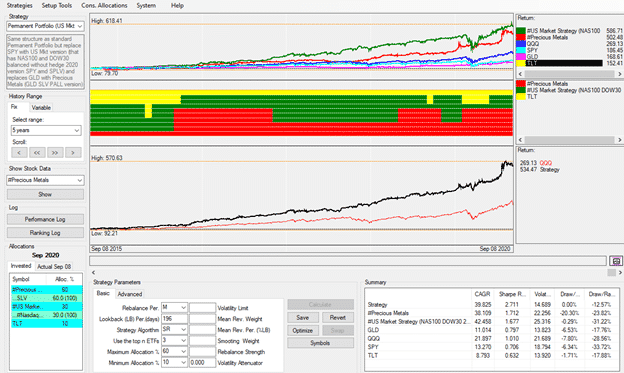

Improving Treasury Hedge

I then tried to find an improvement on the treasury element and replaced TLT with the Treasury Hedge. Despite the TH having similar CAGR to TLT but a much better MaxDD it actually gave a worse result when combined with the PM strategy and SPY. I have found this on multiple occasions when using sub-strategies in a meta strategy in QT; sub-strategy A may have better stats that sub-strategy B but the combo of B with another sub-strategy C gives better stats than combining A with C because B marries with C better. There is no way of knowing this beforehand, so I always have to run multiple versions of sub-strategies with sub-strategies.

Equity – Stock & ETF option

So, the final piece of the picture was to find an improvement on SPY. I tried multiple options of this – QQQ, Nasdaq 100 balanced hedged and not hedged and finally came up with two options; a stock option and an ETF option.

The ETF option is to use the LI US Market Strategy which selects one of QQQ, SPY, DIA or SPLV.

The stock option uses my modified version of the US Market Strategy and replaces QQQ with my version of Nasdaq 100 balance unhedged and replaces DIA with the LI version of DOW30 balanced unhedged and leaves SPY and SPLV unchanged.Both gave excellent results with the ETF version having a CAGR of 33.73 and MaxDD of -12.43 both of which exceeded the targets I had set myself at the beginning of the exercise.

The stock version has a further improvement in CAGR at 39.82 for effectively the same MaxDD at -12.57

When constructing my stock version of the US Market Strategy I did look at using the hedged versions of the NAS100 and DOW30, but these variations all gave worse results. One thing I have found with the LI strategies is that as most of them are hedged, when they are combined into a meta-strategy which itself can also be hedged there can effectively be an overabundance of hedging, so using the unhedged versions of the base strategies will usually give better overall results.

There are probably improvements to be made to this strategy and other testing to be carried out, but it looks to me like it has a reasonable platform for going forward and it did capture the big jump in SLV in July.

You can download a QuantTrader version with all the needed files here: QuantTrader527S Modified Permanent Portfolio.

I would welcome any comments.

Richard Thomas

I have the following strategy that will only Optimize Quarterly. The monthly optimization is all black under any time period? Does anyone know why?

You will need to add the ETF symbol TAIL to run this strategy.

Here is the .ini file:

[StrategyTitle]

0 QQQ Tail Hedge min opt

[StockItems]

#Hedge=#Hedge 1,2,1,1,0.00

TAIL=,2,1,1,0.00,,0,0

TLT=Barclays long term treasury (10 years),2,2,1

QQQ=PowerShares Nasdaq-100 Index,2,1,1

[StockSets]

StockSet95=0 QQQ Tail Hedge min opt,1,3,StockSetStrategy95,2020-09-25,2020-09-25,#Hedge@1,TAIL@1,TLT@1,QQQ@2

[StockSetItems]

StockSet95Item1=1111,StockSet95Item2,0,00000004,2,

StockSet95Item2=1101,StockSet95Item3,1,00000008,2,

StockSet95Item3=0001,StockSet95Item4,2,00000010,3

StockSet95Item4=0100,StockSet95Item5,2,00000020,3

StockSet95Item5=-,-,2,00001000,3,

[StockSetStrategies]

StockSetStrategy95=2,2,Logical Invest Universal Investment Strategy,1101,10,,1

[StockSetStrategyParameters]

StockSetStrategy95=-5,3,176,3,-3,7,-2,7,-6,7,-2,7,0.00,0,-200.00,1,25,1,0.00,0,0.00,0,0.50,1,0,0,0,0,0,0,0,0,0.00,4,0.00,4,0,0,0,4,0,4,0.00,0,0.00,0,0.00,0Topic: UVXY as a hedge option

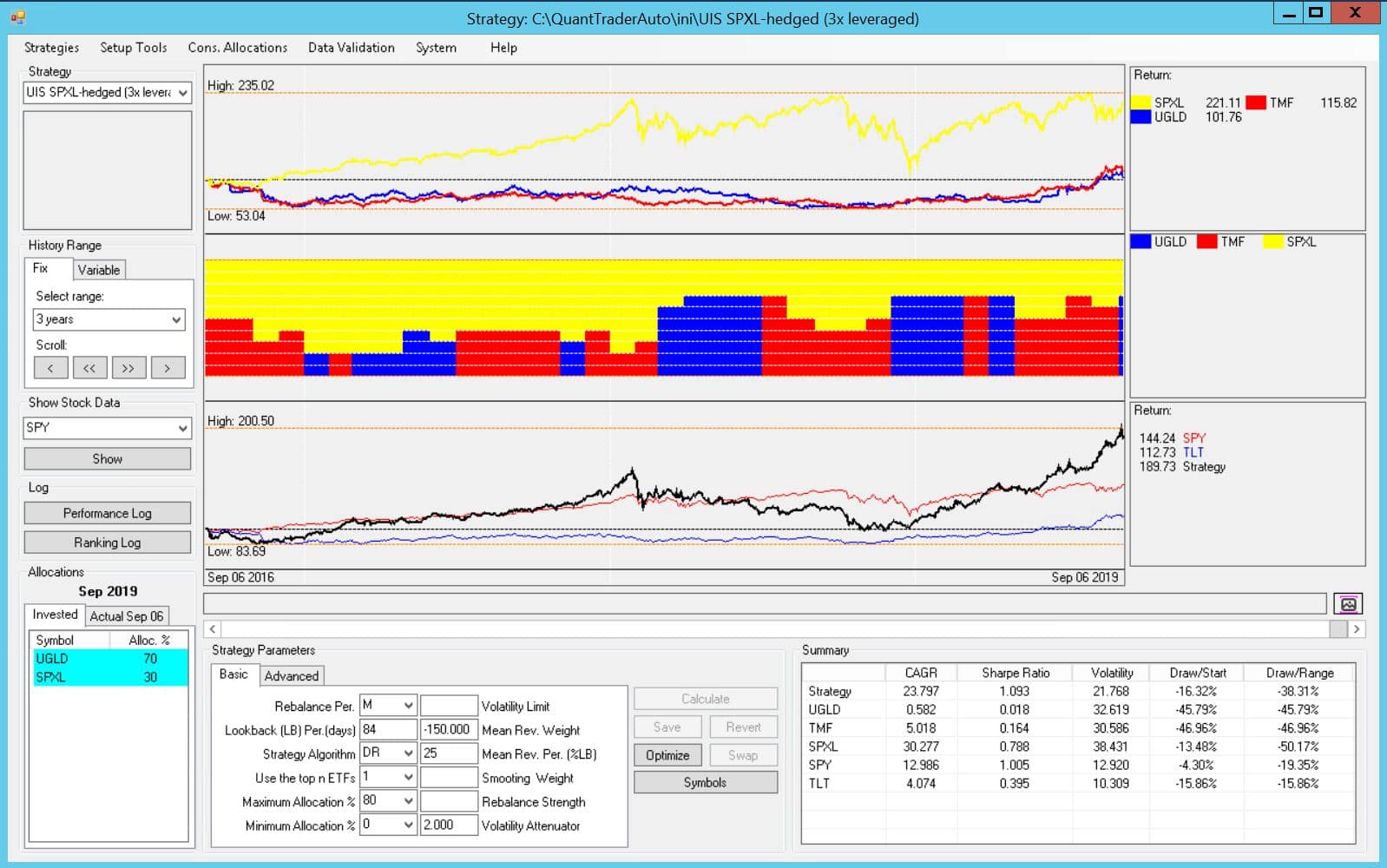

Given that treasuries don’t have a lot of headroom, I have modified the levered hedge to UBT/UGL/UVXY. UVXY seems to be very suited for this role, as it is not a flight to safety item like TLT, but it shows volatility of people fleeing. Have you LI guys looked at something like this in hedging?

I wonder how long TLT will be a good hedge, as real yields are already negative. TLT performed very well during the last years, but there is very little room for yields to go lower. And what could be an alternative to it? Are you already thinking how you would modify your strategies? thank you

Hi guys,

For the performance tables in the pages per strategy at what point is the rebalance struck? So if the HEDGE balanced from TIP to TLT at July month end does your performance table take the % moves as of 31st July close? Or is it 3rd August open?

Best James

Hey guys,

All securities in the strategies are traded on US exchanges and are subject to 30% withholding tax on dividends.

I was thinking to sell before the ex-dividend date to avoid be hit by the tax.

As far as I understand NAV will increase over time and dividend amount subtracted on ex-dividend date prior to open.This strategy should work on bonds like TLT or TIP that actually have their ex-div date on 1st of the month. So selling might make sense as new allocation for next month might not have them in the strategy.

TLT currently has a yield of 2.2% on an investment of 100k that’s 660 of tax.

Granted to the open price on ex-div date might be low or higher due to buying / selling pressure. Fees are not an issue for me as each trade is 1$ with my broker. Any thoughts?

I’ve decided I no longer want to use any leveraged ETFs in my investment strategies. The premise that they actually hedge market risk works, but only sometimes. Their inherent volatility can give you “shock and awe” moments – usually to the downside. ZIV was a trainwreck when the vol trade exploded, and hasn’t been much help since. I have done a lot of thinking about this, and here’s what I think will work best: a “super simple strategy”. It’s similar in premise to the BUG, in that the primary drivers are few, and we stick to the basics – no leveraged funds, SPY/QQQ/CWB as risk assets, GLD, TLT, SHY, and perhaps a few other symbols as “hedges”. The real trick here is that the strategy uses every single cash stop method available, separately, on each and every symbol and sub-strategy, to try to limit drawdowns, which I’ve found to be the real confidence killer.

I begin by making a strategy for each of the foundational symbols that will be used as the primary drivers. These single-symbol strategies are only used to implement volatility limits and cash Sharpe limits, when they make a difference. For example:

TLT 428.44% {CAGR:7.558, SR:0.586, V:12.896, DD:-26.59}

TLT (with stops) 427.41% {CAGR:7.546, SR:0.617, V:12.232, DD:-20.26}Even a tiny “break” on the volatility does make a long-term difference. Sub-strategies are cheap, so let’s go with it. Every symbol we use for the S3 strategy will therefore be “stopped” using a combination of vol and Sharpe limits. So, where to go from here? One idea I’ve had for quite some time is that it might be great to pair bull and bear ETFs for the same symbol. I tested it dozens of ways, and it does work, but only for certain volatility profiles, and you have to use the bear symbols carefully. So, I use this approach for the Treasury and Gold hedges in a simple SRE rotation. To control utilization of the bear strategies, which often have terrible return curves, I increase their volatility multiplier, so the algorithm strongly prefers the bull side. By combining the bull and bear symbols for long-term treasuries (TLT, TBF), I obtain the following results over a 20-year lookback period:

TLT/TBF 698.98% {CAGR:10.228, SR:0.873, V:11.714, DD:-19.32}

Now we’re getting somewhere – this is a good result based upon simple rules. Remember, the goal here is to retain the shape of the treasury curve, so we still retain its “risk off” profile, but to improve upon it as a long-term holding in every possible way. I use the same approach for every symbol in the strategy, and the end result is quite surprising.

In my quest to limit drawdowns, I’ve frequently observed that there are “magical sweet spots” in the optima that produce the best results, but that may be surrounded by poor results. Since we’re playing a statistical game with the future, I will steer clear of those “one off” results on the grid, often choosing lower optima that are surrounded by similar results. If I can find a range of lookback periods that all produce a similar range of results, then I conclude it is a statistically higher probability those lookback periods will be continue to function well in the future. Just a guiding principle. It would be nice to somehow code that as an option in QT, as well as optimizing on other criteria rather than Sharpe – for example the maximum drawdown, which is often much larger than the Sharpe ratio.

Returning to the S3 strategy implementation, my next advancement was to think of ways I could develop a sensible set of “cash stops” that leverage the SR strategy. I’ve observed that combining several similar strategies in a simple SRE rotation can produce better results than any one of them alone. So, we begin with the “base” TLT-TBF rotation strategy, and then implement 2 variants that each use the “CASH” sub-strategy as the only other investment option. One of them is a “low cash” version, where it is limited to 30% allocation, the other is a “high cash” version, limited to 70% allocation. Here are the results:

TLT/TBF low-cash 640.60% {CAGR:9.747, SR:0.905, V:10.774, DD:-17.62}

TLT/TBF high-cash 562.66% {CAGR:9.037, SR:0.910, V:9.935, DD:-17.26}Notice the returns are lower, Sharpe ratios are higher, and the max draw-down in slightly lower than the base strategy without the cash stop rules. Combining the three together in a “Treasury Rotator” (SRE 1 rotation with its own volatility and cash Sharpe limits), the result is:

TLT/TBF rotator 674.58% {CAGR:10.032, SR:0.916, V:10.952, DD:-20.00}

It turns out the SRE strategy really only uses the basic TLT/TBF and TLT/TBF high-cash variants. Also, the results are good but not great compared to the simple TLT/TBF rotator, so you might think it’s not worth all the effort. However, other symbols respond better to this approach. Also, let’s compare the end result to a simple TLT holding, and to the built-in “Treasury Hedge” strategy in QT:

TLT 428.44% {CAGR:7.558, SR:0.586, V:12.896, DD:-26.59}

Treasury Hedge 420.39% {CAGR:7.456, SR:0.792, V:9.417, DD:-18.49}

TLT/TBF rotator 674.58% {CAGR:10.032, SR:0.916, V:10.952, DD:-20.00}Since we’re using this strategy as a hedge, and we’re hoping the “rotations” we apply at higher levels of the S3 strategy eliminate some of the draw-down, I’m generally happy with this result. Here’s the results for Gold (GLD/DGZ):

GLD 552.83% {CAGR:8.94, SR:0.509, V:17.568, DD:-45.56}

GLD-USD (QT built-in Gold strategy) 595.31% {CAGR:9.345, SR:0.732, V:12.774, DD:-28.22}

GLD/DGZ Rotator 988.69% {CAGR:12.158, SR:0.871, V:13.957, DD:-18.53}Not too shabby. Let’s see what happens when we simply combine the Treasury and Gold rotators into a simple SR2 strategy with minimum allocation 40%. Since these two strategies move in very different ways, the SR strategy can make quite effective use of the two by varying their allocations between 40-60%. Compare this to the QT built-in “Hedge” strategy, which uses a similar combination of Gold and Treasuries:

QT Hedge 543.39% {CAGR:8.846, SR:0.771, V:11.481, DD:-24.04}

S3 Hedge 897.16% {CAGR:11.614, SR:1.284, V:9.044, DD:-10.05}Wow, that’s a hell of a good result, isn’t it?

Let’s see what happens when we do the same thing for QQQ, the Nasdaq-100 index fund from PowerShares. There is a Nasdaq bear ETF (PSQ), but I didn’t bother with it. In this case, all I do is take QQQ and implement the various cash stops to it directly. There is a base strategy for QQQ alone, and then one that uses a 30% cash stop, and a third that uses a 70% cash stop. Optimized over a 20-year timeframe, here are the results:

QQQ 345.27% {CAGR:6.402, SR:0.232, V:27.548, DD:-82.97} Holy sh%t that’s a serious drawdown! If only we had simple cash stops in place…

S3 QQQ with simple cash stops 819.14% {CAGR:11.107, SR:0.529, V:21.008, DD:-56.16}

S3 QQQ Rotator with full cash stops 1447.55% {CAGR:14.320, SR:0.865, V:16.551, DD:-21.99}Wow! That’s something else, isn’t it? I happen to like the SPLV S&P 500 low-volatility symbol as well, so using the same approach with that symbol:

S3 SPLV Rotator 2164.61% {CAGR:17.468, SR:0.889, V:19.644, DD:-29.09}

Why not just flip-flop those 2 strategies against each other in a simple SRE?

S3 QQQ-SPLV Rotator 3981.46% {CAGR:20.302, SR:1.151, V:17.634, DD:-18.63}

Sweet result. I’ll cross my fingers and hope it comes true. Lol. Anyhow, back to reality. Let’s combine the S3 TLT/GLD and QQQ/SPLV strategies into a single S3 Risk strategy:

S3 1475.39% {CAGR:14.522, SR:1.650, V:8.8, DD:-11.66}

Comparing this result to the underlying symbols:

TLT 428.44% {CAGR:7.558, SR:0.586, V:12.896, DD:-26.59}

GLD 552.83% {CAGR:8.94, SR:0.509, V:17.568, DD:-45.56}

QQQ 345.27% {CAGR:6.402, SR:0.232, V:27.548, DD:-82.97}

SHY 140.33% {CAGR:1.998, SR:1.425, V:1.403, DD:-2.23}You would never think you could do that with those ingredients, would you? Let’s see what a simple SR3 rotation with a 60% maximum allocation would yield, without all the fuss of the cash stops and limits and such:

TLT/GLD/QQQ/SHY (SR3, 60% max, SHY 20% max, 102d LB) 699.68% {CAGR:10.343, SR:1.188, V:8.703, DD:-10.92}

Eliminating SHY:

TLT/GLD/QQQ (SR3, 60% max, 98d LB, -150%MR, 25d MRP) 945.16% {CAGR:11.906, SR:1.435, V:8.298, DD:-12.41}

And the QT Permanent Portfolio (TLT, SPY, GLD) for reference:

QT Permanent Portfolio 748.29% {CAGR:10.605, SR:1.381, V:7.679, DD:-13.37}

Overall, very similar results, though the QQQ variant is an improvement. I would suggest that change to the Permanent Portfolio in QT. Not too bad overall, considering we’re only using 3 symbols, with no cash stops at all. The “dumb” S3 plows right through the 2000 and 2009 meltdowns with aplomb. Wouldn’t you have killed for that back then?

Still, implementing some cash stop-out rules and using a few extra rotation strategies, here is the result:

S3 with stops: 1475.39% {CAGR:14.522, SR:1.650, V:8.8, DD:-11.66}

S3 without stops: 945.16% {CAGR:11.906, SR:1.435, V:8.298, DD:-12.41}It’s been a worthy exercise, I’d say. A definitive improvement to the Permanent Portfolio that nearly keeps parity with a simple QQQ investment since 2009 (albeit trading costs would drag performance), but with less than half the volatility and a third the maximum draw-down. Here are the 10-year results compared to QQQ:

S3 482.23% {CAGR:17.060, SR:2.103, V:8.112, DD:-7.33}

QQQ 502.18% {CAGR:17.536, SR1.010, V:17.355, DD:-22.79}Of course, we know it’s not too easy to keep up with QQQ during it’s best rip in decades while maintaining a hedged portfolio with full cash stops. And, those stops are going to come in extremely handy the next time the market decides to go into nuclear meltdown mode, which will come sooner or later.

Interestingly, we can improve upon these results still. If I add a similar strategy based upon the impressive CWB fund, and then also include one based upon the Global Markets Rotation Strategy (after giving it the old “S3” treatment) to improve upon the GMRS Hedged strategy results, an S3 Risk Rotator returns the following:

S3 Risk Rotator 1422.32% {CAGR:14.569, SR:1.871, V:7.785, DD:-7.52}

It’s an ok improvement I guess, it does cut the vol and draw-down a bit by incorporating CWB and GMRS. How about the real deal though? Starting in October, I’ll be using the S3 strategy, but I will combine it with the granddaddy of them all, the Nasdaq 100 top 4 “N4” strategy. The issue with N4 is of course the volatility. Also, since it picks 4 stocks, it poses a very focal risk. Therefore, I never allocate more than 20% of my total portfolio to N4, since any single stock should never really comprise more than 5% of your total holdings. Also, I will examine the individual symbols and often choose ones further down on the list if their returns look a bit more stable. I also like to avoid holding stocks if they are going to announce earnings during that monthly investment period. Earnings can often deliver a wicked down-side surprise, and I just don’t need any of that nonsense. So, what does this thing look like in an S3-N4 combination? We’ll call this the “real” S3 strategy, so here it is:

S3 3244.38% {CAGR:21.315, SR:2.253, V:9.462, DD:-8.74}

Hell yah, that’s what I’m talking about. Now, my personal implementation of this also includes one more little secret surprise that I don’t feel like sharing right now, but if you follow this same recipe, you will arrive at similar results. Happy QT’ing y’all!

:)

Tom

Topic: February 2018 correction

I’d like to discuss correction that we’re all witnessing now. I don’t want to spread fear but talk about whether we should do anything about it or rather keep going as usual.

The hard facts are:

1) We experience severe drawdown (in just few days it exceeded 5 years max DD for most strategies) – and there is a (quite high in my opinion) possibility that drawdown will deepen

2) Our hedges are not working very well (TLT/TMF doesn’t work at all, GLD is not much better, only thing that kind of works is EUO)

3) The correction started at beginning of the month after very good January, so our strategies are at nearly full-risk mode.It’s hard to predict right now if it’s “healthy” correction and everything will go back to “normal” (or some “new normal”) or it’s just a start of some longer bear market.

So, what can we do about it? First idea is to do nothing, just wait for the month to end and then rebalance portfolios as usual. One can also think of adding risk to portfolio (to recover faster) or switch to less risky one (to be more drawdown proof), even to go fiat.

What I’m considering right now is rebalancing earlier, near 15th Feb. From what I see it’s enough time for the strategies to adjust a bit. The thing is even if strategies are slowly allocating less to risky assets, the rebalancing will rather not lead to having lower allocation of risky assets in portfolio. Eg. even if SPXL allocation goes from 80% to 70% when running QT now, SPXL went down more than 20% during last week, so we’d actually have to buy more of it.

What are your thoughts? Are you going to do anything?

I would be interested in hearing how subscribers are adapting their portfolios in light of the new hedging strategies, particularly their allocations to MYRS, UIS3x and Nasdaq since they use hedge3x. If I understand the parameters of these updated leveraged strategies correctly, it looks like there is the potential for the new MYRS and Nasdaq 100 to be 100% in UGLD. (hedge3x max allocation 100% and UGLD max allocation within hedge3x 100%) UIS3x hedge3x is max 80%.

Since 2012 UGLD has maintained only a small allocation in these strategies, but that’s not a very long lookback and only in a low volatility bull market. The regular hedge strategy has a very different structure and not just because it is unleveraged. It uses currencies and maintains a minimum allocation of 20% to TLT, if I am understanding the QT parameters correctly. My concern is that the new strategies probably look very different prior to 2012 and may in fact diverge sharply from the unleveraged strategies in a bear market. I want to know how hedge and hedge3x would have performed within these strategies outside of this bull market.

Search Results for 'tlt as a hedge'

Viewing 69 results - 1 through 69 (of 69 total)

Viewing 69 results - 1 through 69 (of 69 total)