Home › Forums › Logical Invest Forum › Why is UISx3 Switching to 70% UGLD for September 2019?

- This topic has 15 replies, 9 voices, and was last updated 6 years, 5 months ago by

Alex @ Logical Invest.

- AuthorPosts

- 08/31/2019 at 8:37 am #69786

RB

ParticipantThe 3X Universal Investment Strategy (UISx3) is switching to a 70% UGLD position for September 2019.

UGLD had a very large gain in August 2019.

Given the likelihood of reversion to the mean, I’m afraid a 70% UGLD position will result in losing the wonderful YTD 2019 gains in UISx3.

Why is UISx3 switching to such a high % UGLD in September 2019?Thank you,

Ron08/31/2019 at 9:43 am #69797robininni

ParticipantI don’t have an answer for you but I just posted a very similar question about the Moderate Risk Portfolio changing to a huge allocation in TLT now for September after TLT just had an incredible 10% run in August. It seems we are chasing profits and I hate to put emotion into it, but it seems like a 54% allocation to TLT NOW is not wise. You concern with UGLD is even more alarming.

08/31/2019 at 10:39 am #69798ParticipantThank you. It’s nice to know I’m not alone.

The only thing I can think of is that interest rates may continue going down because the ECB is expected to cut rates in September, and then the Fed would lower as well. Hopefully I’m wrong, but I think the best case scenario is that we lose a lot in TLT/UGLD before the ECB September meeting, we gain some after the meeting, and end the month flat.

This is one of those times when I really don’t like the Logical Invest strategies…emotions start to mess things up, which as you mentioned is not good.

08/31/2019 at 11:32 am #69799Vangelis

KeymasterThe 3x UIS Leveraged strategy is an extremely risky strategy and should not be utilised by itself. It should make you uncomfortable to trade it. The model provides recommendations so if it sounds too risky or does not sense you should not follow it until you gain some faith in it.

That said, the model uses rules. According to those rules it thinks it’s best to go UGLD/SPXL rather TMF/SPXL which makes sense as gold had a better risk adjusted performance. The problem with UIS3x is that even it’s most balanced allocation, 50% TMF – 50% SPXL, is extremely risky unless used in a small account that can withstand -40%+ draw-downs.08/31/2019 at 9:04 pm #69874Anonymous

InactiveAnyone who has invested in this strategy all year are up nearly 80% YTD. That’s incredible. It’s almost better than 12 years of regular market investing.

If you are nervous going forward, and rightly so, there is nothing wrong with going all cash and taking a break for the rest of the year. After all, you are up nearly 80%.

For me, I will reallocate based on the monthly signals and trudge on, win or lose, but as history has shown, it’s winning way more than losing.

08/31/2019 at 11:38 pm #69882ParticipantGood point, Deshan.

You’ve given me a lot to think about this weekend before the market opens on Tuesday.

Thanks,

Ron09/01/2019 at 10:19 pm #69975Mark Vincent

ParticipantThe strategy Max drawdown is 50%. That means your investment is cut in half very quickly. On the upside the likelihood of both stocks, Gold and bonds going to zero is almost zero. If you have a long term horizon and nerves of steal this strategy will work but it’s hard to swallow a 50% loss.

09/07/2019 at 11:40 am #70276R D HATHCOCK

ParticipantIMO–UIS 3x was a problem once the fed started hiking rates as TMF, which was the old standby hedge favored by falling rates, was getting crushed along with SPXL. It was the worst of both worlds. I recall they added UGLD to get disconnected from interest rate dependence. However, once the FED started cutting rates, then TMF worked properly again. So, as long as they hold or reduce rates further, TMF is a wonderful hedge for SPXL.

The same thing happened to the MYRS. Volatility spiked so ZIV plummeted, and the TMF hedge worked backwards of the strategies intent. I held money in both strategies when they went south.

My personal view of UIS 3x and MYRS is to allocate to each like they are small cap stocks.

09/08/2019 at 1:30 pm #70343Alex @ Logical Invest

KeymasterYes, that’s exactly what happened. Now with the hedge being able to pick from either bonds, IPS and gold it looks better suited going forward, as it should adapt to whatever happens with bonds long term.

I also want to stress again that UIS3x and MYRS should only be used as a small part of your overall portfolio, they are extremely aggressive.

09/08/2019 at 2:20 pm #70344ParticipantThanks RD.

09/08/2019 at 2:23 pm #70345ParticipantAlexander,

Can I please get your input on my original question? Why is UISx3 Switching to 70% UGLD for September 2019?

Is the strategy switching to gold simply because it’s the lesser of two evils (TMF and UGLD)? The part which doesn’t make sense to me is, if you know you’re going to lose money in both TMF and UGLD because of reversion to the mean (after such a large upside move), why are we investing in either ETF?Thanks,

Ron09/09/2019 at 4:04 am #70349KeymasterHi Ron, see my reply here, probably would have been better in this thread: https://logical-invest.com/forums/topic/moderate-risk-new-allocations-for-september-tlt/#post-69843

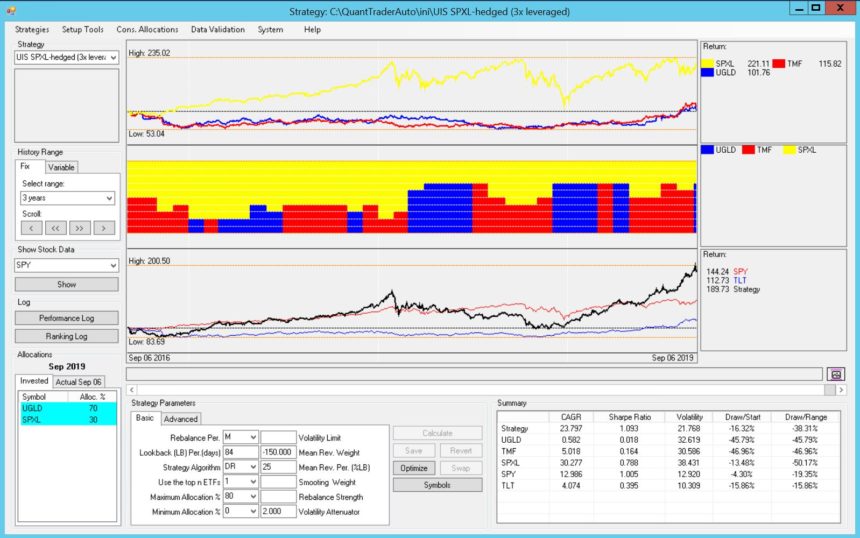

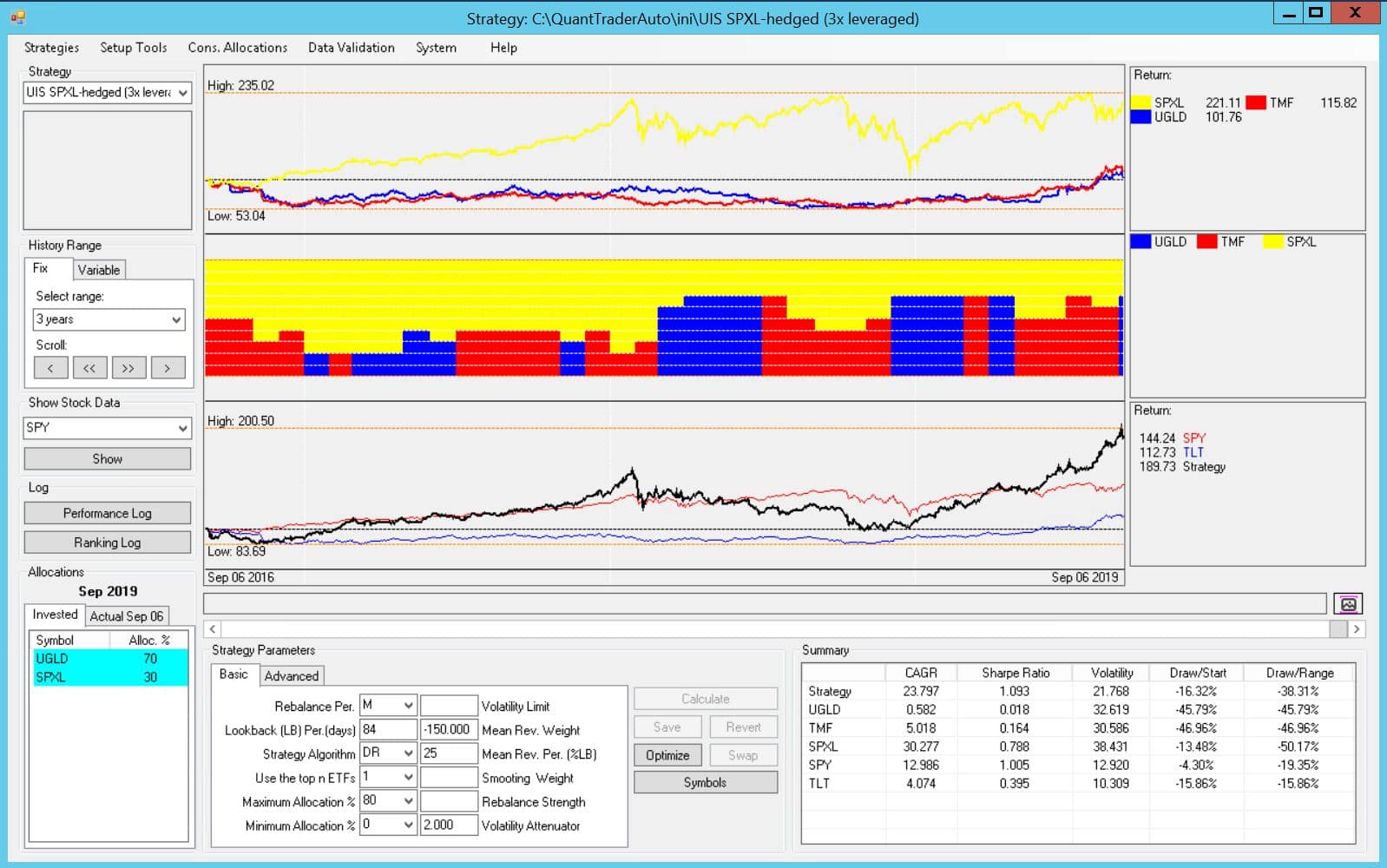

With the 70% allocation to UGLD the strategy is basically in “risk-off” mode, and picks the better of UGLD and TMF, or the “lesser of two evils” as you say. I posted two screenshots from QT below, one for the 4 months look-back period and a 3yrs for the big-picture.

Technically speaking, the strategy considers a volatility attenuator of 2, which means it is very sensitive to any change in volatility, and that’s what we’ve seen for quite some time now, basically since Q4 2018 the hedge was 40-70% of the allocation. Also it considers the reversion to the mean, basically it ignores or even penalizes the performance of the last month (based on the parameters performance is calculated as Performance last 84 days – 150% performance of last 21 days (25% of lookback)).

As I referred to in the other thread:

“That’s the psychologically tough part of Momentum driven strategies: Buy when things have already moved quite a bit, sell even if you think the party might re-start.However, we’re late in the cycle, and despite the ‘bit’ of volatility recently we’ve not seen any serious correction yet, were the flight to safety moves such safe-haven prices much more violently.

Just some days ago replied to a comment re how negative yields feel like in Europe, so who says the 1.5% in the US is the bottom? See the comment by Vangelis today what it would take to devaluate the USD rate-wise.

If you feel uncomfortable with long term bonds or gold, the signal basically says ‘risk-off’. Cash is an alternative, even if historically in our models you’d lost some of the performance.”

4 months:

3 years:

10/01/2019 at 7:30 pm #71695

10/01/2019 at 7:30 pm #71695Invest

ParticipantIs always interesting to know the reason why a strategy like this invest in this or that asset class at the moment.

And there is always a difference if you follow a strategy or your opinion or experience if you follow a strategy like this is much easier to keep emotions out.

At the moment I personally stay away from Gold as a hedge since the big money is „all in“ it’s possible to dry up and recession fear and the trade war ist already priced in.

I General like gold as a hedge

but also prefer to buy at the bullion market eater than the ETFs expect the leverage one for this strategy.11/02/2019 at 12:48 am #73152InactiveNo harm, no foul. The October gains offset the September losses. Now back to bonds.

02/01/2020 at 4:14 pm #77572DWoods

ParticipantThis strategy continues to deliver solid returns and is, by far, the best performer LI has produced overtaking the MYRS as #1.

In a perfect world, having one million dollars invested in this stategy would seem plausible, but reality is real. So I personally wouldn’t want that amount invested so aggressively and I’m sure others would agree. So I found comfort in using a base amount each month that theoretically produces an amount most comfortable for me based on CAGR and putting the monthly gains into a cash account that draws 2% APY when the rebalance is positive, which has been quite frequent lately. No complaints here.

Thank you guys for keeping this strategy alive and well. It’s perfect for me and anyone with a true taste of aggressive investing.

02/02/2020 at 10:24 am #77576KeymasterIf I wouldn’t know, I’d now guess the “D” stand for “Daredevil” Woods :-)

Actually pulling profits into a different account is a smart rebalancing approach.

- AuthorPosts

- You must be logged in to reply to this topic.