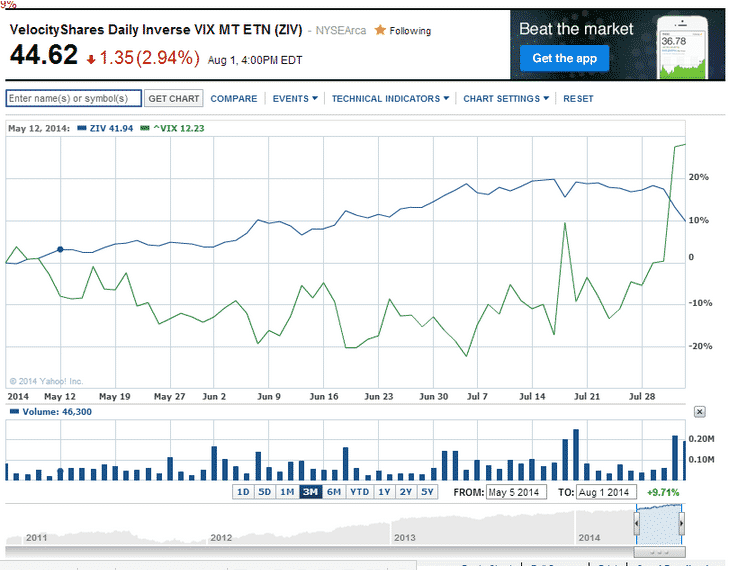

This monthly premium of being short volatility is the only thing which makes the ZIV price go up. Unfortunately there is a second quite strong influence on the ZIV price. This is the market volatility (VIX). In the chart below you see the green VIX chart. Every spike corresponds to a fear spike of the investors. During such spikes we also have smaller market corrections. During these market corrections ZIV is going down, because the ZIV holders play the role of the insurer and they have to cover the losses of the insured investors.

The good thing is, that the 3% monthly premium of short volatility investments normally more than covers all possible losses of the investors. 3% per month is 42% per year. In fact we borrow investors money to cover their short term portfolio losses at the enormous rate of 42% interest per year!

Continue benefitting from Short Volatility

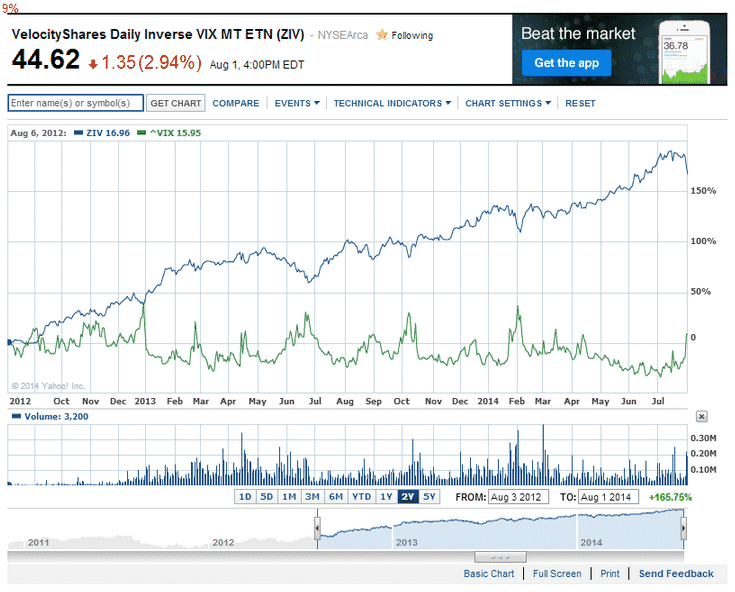

The influence of the VIX short volatility can be considered as a sort of noise which adds to the quite stable premium performance of ZIV. The good thing is, that this volatility is mean reverting, so that even if ZIV has an intermediate drawdown, you know that this is only a temporary drawdown.

The last few months, the VIX level was extremely low, therefore also the benefit from being short volatility. Now it is up again at 17 which can be considered as quite a normal average level. So there is no immediate danger because of this VIX level. Only if VIX comes in the region of between 20 to 25, then time comes to exit a ZIV position.

Current Short Volatility environment

If you look at the 3 month chart below, then you see that ZIV is still up nearly 10% for the last 3 month. Seen that we get only about 3% premium per month from being short volatility which makes about 9% for this period, this is still at the upper level of the normal performance. The nearly 20% intermediate performance was only due to the drop of the VIX level in July. In fact this was rather noise and not something which could be considered normal.

Even if ZIV goes down another 5%, this is still perfectly normal in the history of short volatility. You don’t need to be afraid of this. Also you always have to bring these price corrections in correlation to the current market situation. Most of these corrections did not have economic reasons, but the have been the result of political problems. Until now such political problems have always been always short lived.

At the moment, we only hear positive news about the US economy and also Europe is doing quite well. The stock market correction and also the ZIV correction of end July is a normal event which just happens like this every 2-3 month. We had about 10 such events during the last 2 years. Such events are normally the best moments to build up your ZIV position (in short volatility). However it is important that you don’t invest 100% of your capital in an ETF like ZIV. Invest also a part in safe Treasuries. These have normally an inverse correlation with ZIV and this allows you to do some rebalancing (sell Treasuries high and buy ZIV low) during such a volatility spike.