A hedge is always an investment which is negatively correlated to the main investment. When the main investment goes down, the hedge should go up and if the main investment goes up, then the hedge normally goes down. It is clear, that we like the first, which is to reduce the draw downs with a hedge, but not to reduce the gains.

If you have a stock portfolio, then the main hedge possibilities are:

- A VIX ETF like VXX or a VIX Future. These have nearly a -1 correlation.

- An inverse ETF on a index like SH which is the inverse of the S&P 500 SPY ETF

- Precious metals like GLD or SLV

- Treasuries

A lot of people use 1) and 2) to hedge their positions. This may probably make sense if you have a big stock portfolio, and you can not sell everything instantly in case of a market crash. These two must be perfectly timed. I do not think it makes sense to use them as a hedge for longer periods because the VXX ETF has an extremely strong down trend of about 5-10% per month. This is a very effective but also very expensive hedge. Such a hedge will ruin the performance of your portfolio if you keep it longer then one or two weeks. Same with SH. Because the S&P 500 has a long term up trend of about 8%, you will lose about these 8% per year if you use SH as a long term hedge.

Precious metals 3) are much better. They are a safe haven investment. They normally have an inverse correlation to the stock market in times of trouble and on the longer term they should go up at least because of inflation. Gold and Silver are today priced about at their production cost. Sure, it is possible that they go down below today’s prices for a short time, but the down potential is very limited versus the up potential. Mining costs are increasing quite fast and on the long term GLD and SLV will go up at least 5% per year. If you have a Forex trading account you can borrow GLD or SLV for about 0.5% interest today. So it is very cheap to hold these precious metals. I hold quite a big position in Silver and the last months have shown, that this is quite a good hedge. Always when the US market is down, then GLD or SLV goes up.

Treasuries 4) are also a good “safe haven” hedge, even if the Fed’s tapering process is still ongoing. At the moment treasuries are showing a very constant negative correlation with the stock market. If you add a treasury position to your stock market position, then you can reduce the draw-downs quite a lot. The good thing with Treasuries compared to an inverse S&P500 ETF or a VIX ETF is , that on the longer term they go up by about 4% per year. If you can invest in Treasuries by shorting an -3 inverse TMV ETF, then in addition to these 4% you profit of an additional time decay and the high management fees of this ETF. The TLT ETH is down 2.1% for the last 24 month. Our TMV ETF is down 19%. If you short it then it is up 19%. Because it is 3x leveraged compared to TLT you have to divide by 3. So, compared to TLT which is 2.1% down it is 6.3% up. This is a 8% difference to TLT.

So, overall the TMV hedge is really the best thing you can do. This ETF reduces your draw-downs and on the long term it should return about 10% per year.

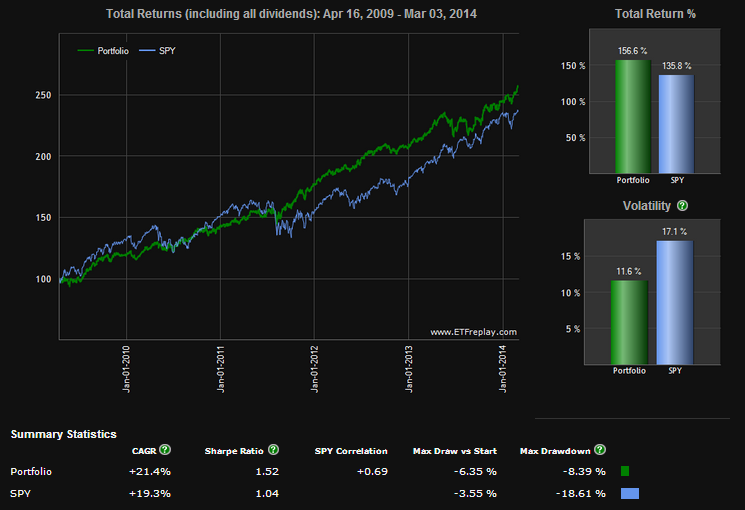

I proposed to invest 25% (=80%+20%) of your stock market investment in such a hedge. Here is a comparison of a hedged SPY portfolio compared to only SPY.

As you can see, such a TMV short hedge is one of the best things you can do. Increased profit and much less volatility and this with the year 2013 included, which was one of the worst years for treasuries ever. One of the most important things is, that it will reduce the max. draw-down by about 50%.

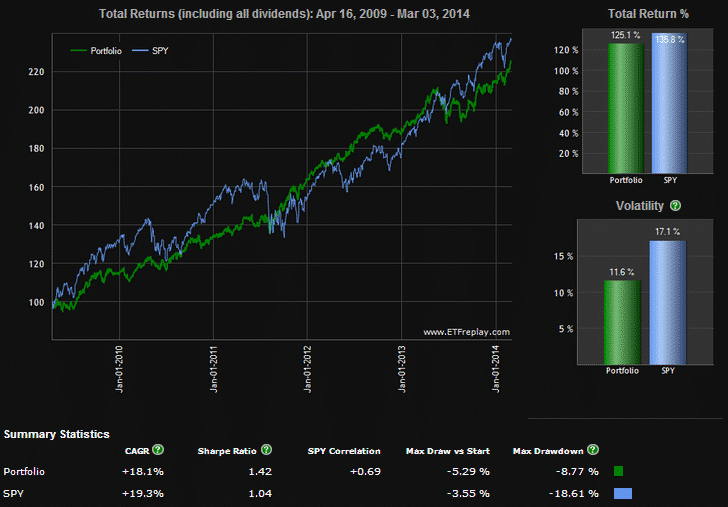

If you can not short TMV, then you can also go long TMF.

The result is still much better then just a normal SPY investment in the stock market . The return is slightly smaller then SPY alone, but the risk (volatility) is reduced by 1/3rd.

In general it is quite easy to find out if it makes sense hedging a portfolio. You just have to calculate the Return to Risk ratio (Sharpe Ratio) of the portfolio without and with hedging. If it is bigger with hedging, then your hedging makes sense. In general only a hedge with Treasuries or precious metals will increase the Sharp ratio.

One of the biggest advantages of such a hedge is that it is always in place. Even if something really bad happens over the weekend, like now the Crimean/Ukrainian crisis and the next Monday the stock markets open with big losses, then you can be happy. A 20% hedge in TMV or TMF will cut your draw-down by 50%. If you are rather a risk adverse, then you can also increase such a hedge to 30%. This will nearly flatten out any bigger draw-down.

I find your argument regarding using inverse treasury ETFs compelling. However, I was wondering how this strategy would have performed in other market regimes than the one since 2009, which is when TMV came into existence. Is it possible to test this strategy using a synthetic version of TMV? Also, if one were to use this strategy with leveraged ETFs, (for example, QLD or TQQQ) do you think that the percentage of the hedge should be increased?

Again, many thanks for the excellent work.

Seems most (if not all?) brokers have leveraged ETFs and ETNs on the “hard to short” list – meaning that they will charge you an annual fee (2-5% depending on the broker) for the service of “finding” the stock to borrow and to borrow them. For TMV I got special deal of 2% with Schwab but other I speak to get as high as 7-8% offered. You do not seem to incorporate this fee into your return calculations?

If the yearly borrowing fee is below 4%, then it makes definitely sense to short these -3x leveraged ETFs. These ETFs have an additional 10%-40% return just because of rebalancing/compounding losses even if the market is flat.

It appears that you must close out the tmv short often and immediately reshort it in order to optimize. SeekingAlpha discussed this in an article by Cliff Smith in his chat. Every 10% in profit is the best trigger pt. for closing and reshorting. Would you please address this issue?

I do not short as much anymore, but on Interactive Brokers, where I did a good amount of short positions, IB would mark to market everyday, and release (or take) margin and liquidity based on the current position value. Not sure why I would want to deal with commissions/slippage, and trade management any more frequent than necessary.

My margin interest is 3.25% and “hard to borrow fee” is 2% for a combined 5.25%.

Should I use short TMV or TMF?

Cheers! Ben

I would always short TMV. You get about 10% more profit per year. I am not sure about the margin interest, but I think this one you have to pay anyway.