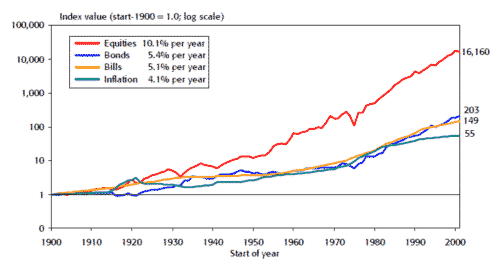

Bond investing doesn’t get much attention in the retail investing arena. But bonds can form an important function within a retail investors portfolio. They can generate income, as well as capital growth and lower the overall volatility of an investor’s overall portfolio.

What is a Bond?

A bond is a form of IOU that pays interest. Before the world went digital, bonds were certificates with a nominal, or face, value, an interest rate and a set of dated coupons which could be torn off. Each coupon was torn off on its respective date and mailed to the issuer. In return, the owner would receive a check for the interest rate as a percent of the face value of the bond. When the bond reached maturity, the owner mailed the final coupon to the issuer and received the face value and the final interest payment in return. Everything is electronic these days, but the system works the same, and the interest payments are still known as coupons.

Bonds are issued by governments, municipalities, and companies. They usually have maturities ranging from a year to 100 years – in fact, some bonds never mature. Bonds with very short maturities are known as money market instruments.

Bond Maths

Yes, bond prices do go up when interest rates go down and down when interest rates go up. Bond Maths seems complicated, but with the aid of a simple example, you’ll see that it isn’t.

Bonds are initially sold in an auction and after that, they are traded on the ‘secondary market’. That means they are not necessarily sold at their face value. Let’s say you buy a bond worth $100 with a 5% coupon and maturity date 10 years in the future. If you can only earn 4% elsewhere you may be prepared to pay slightly more for that 5% coupon.

If you were to pay $106 for that bond you would still receive a coupon of $5 (5%) every year, which would be 4.7% of the $106 you paid. But that would still be more than the 4% you could earn elsewhere. When the bond matures you will receive $100 back, even though you paid $106. So that $6 capital loss needs to be factored into the interest you receive. The total yield or ‘yield to maturity’ would then fall to 4.25% – but that is still more than 4%, so you are still happy to pay $106 for the bond.

Now let’s say interest rates rise to 6% and you decide to sell the bond. Well, you are going to have to sell it at a price that yields at least 6%. It turns out that if you sell the bond for $92.60, it will yield 6.01% for its new owner. They will be earning a $5 coupon on a $92.60 investment which is 5.4%, and they will also make a $7.40 profit when the bond matures. So that’s why rising interest rates mean bond prices fall and visa verse.

What affect bond prices?

The primary driver of bond prices is interest rates and expectations of where interest rates are headed in the future. Interest rates, in turn, are manipulated by central banks to control inflation and to stimulate growth. So, bond prices tend to be driven by the way the market interprets economic data and commentary from central bankers and politicians.

Currency movements also affect interest rates, as do geopolitical events. If a currency is very weak the central bank may want to raise rates to attract flows into that currency. Bonds are seen as a safe haven during times of uncertainty so they appreciate when stock market volatility increases and when geopolitical events occur.

The other factor that affects bonds is the credit worthiness, which is the issuer’s likely ability to pay back the principal of the bond, along with the interest payments. The more risk an investor takes, the more they need to be compensated and, therefore, the higher the interest rate they will demand.

Types of Bonds

Bonds are issued by governments, government agencies and parastatals, municipalities, and corporations. Government bonds issued in the currency of that country usually have the highest credit rating and pay the lowest interest. If a government issues bonds in a foreign currency, their obligations will carry currency risk, which will make them riskier and they will pay a higher interest rate. Corporate bonds vary widely in terms of credit worthiness. Bonds issued by corporates can also have varying levels of seniority – that means that in the event of the company being liquidated, some bond issues may be paid out before others. Convertible bonds are corporate bonds which can be converted into equity.

High-yield, or junk bonds, are bonds that are not rated investment grade by rating agencies. Not all junk bonds are very risky. If a bond is rated investment grade, it has a probability of default of around 2-3%. Everything else is rated as a junk bond, even if the probability of default is as low as 4%. So junk bonds actually cover a wide spectrum of risk.

How to invest in Bonds

Bond investing used to be quite complicated and was only accessible to people with $50,000 to invest. Nowadays though, most discount brokers allow clients to invest in bonds. The other alternatives are a mutual fund or bond ETF. There are now over 320 bond ETFs to choose from. Some invest in very specific types of bonds, while others offer a diversified portfolio of bonds. One of the best known is the TLT ETF issued by iShares, which invests in US Treasuries with an average maturity of 20 years. The TLT ETF is popular with active traders, but can also give long term investors exposure to US Treasuries.

Other well-known bond ETFs include:

- SHY, another iShares ETF which invests in US treasures with a maturity of 1-3 years. ETF rotation strategies often use this ETF to ‘park’ money during times of uncertainty.

- PCY, issued by PowerShares, is a bond ETF that invests in emerging market government bonds.

- CWB, issued by SPDR, invests in convertible bonds

- JNK, also issued bt SPDR, invests in high yield bonds

Logical-Invest’s Bond Rotation Strategy rotates funds between some of the ETFs listed above to achieve consistent and stable returns. This is a sensible, low-risk method of allocating capital to bonds.