The Logical-Invest newsletter for September 2019

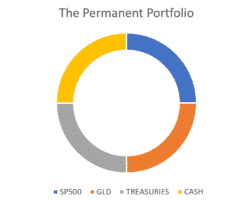

Fear of a coming recession? And yet this is the perfect environment for a Logical Invest strategy. Our top performers for the month were the Leveraged Universal Investment Strategy (+19.9%) and the Maximum Yield strategy(+ 10.3%). Even our free Enhanced Permanent Portfolio returned 5% in August. Why? The answer is in the “safe-haven” assets: Bonds and Gold. Just this month, TLT is up by 11%, GLD by 8% while the SP500 lost -3%. Our strategies … Read more